You may have seen news stories about “Trump Accounts”, a new type of investment account aimed at building wealth for children. Today I’m writing a quick explainer on how they work, rules and restrictions, and eligibility for receiving funding from the government or others. First off, here is a quick graphic breaking down the key points and rules of the Trump Accounts:

Opening and Withdrawal Rules

The Section 530A accounts, more commonly known as “Trump accounts”, were created as part of the One Big Beautiful Bill Act (OBBBA) as a type of individual retirement account (IRA) for eligible children. Any child who does not turn 18 years old within a given calendar year is eligible for a Trump account. The accounts will grow tax-deferred similar to existing IRAs but will have a smaller variety of investment options than traditional IRAs; specifically, there will be an approved list of index funds for Trump accounts although the list has not yet been finalized[3].

The child for whom the account is opened is legally considered both the beneficiary and the owner; These accounts will not allow for distribution (withdrawal) of funds until the beneficiary turns 18 with a few exceptions mostly related to rolling the funds into a different Trump account. Once the owner turns 18 years old, the account is treated like a traditional IRA account, meaning any withdrawals will be subject to ordinary income tax and an additional 10% penalty if the withdrawal is before age 30, unless the withdrawal is for a qualified exception. The two main qualified exceptions are:

- Qualified higher education expenses

- First home purchase

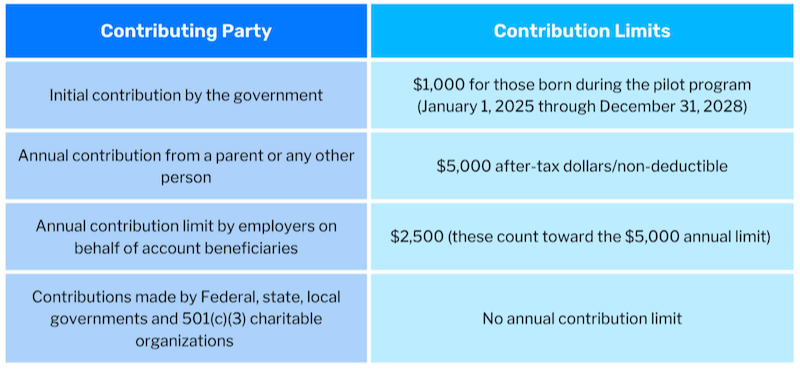

Contributions

There are a few options for funding these accounts. Every account may be funded up to $5,000 per year, and the contributions to the accounts are tax-deductible to the individual making the contribution. Employers are allowed to contribute up to $2,500 per year to these accounts, but it is important to note these contributions count towards the $5,000 cap per year.

There are two additional federal contribution options. The first is a one-time contribution of $1,000 to accounts owned by children born during the calendar years of 2025-2028. The second is a program generously funded by Michael and Susan Dell through a $6.25 billion donation to the program. This program will offer $250 to any child under 10 years old who does not qualify for the $1,000 federal stipend as long as they live within a zip code where the median household income is less than $150,000[4].

There are still some rules and regulations to be decided before these accounts go live. The accounts themselves can be opened starting now but are not eligible to be funded until July 4th, 2026. If you have any questions on opening or planning for these accounts, please reach out to us here at Eternal Wealth Management and we will be more than happy to help.