“The best way to predict the future is to create it.”

-Abraham Lincoln

Here’s what you need to know this week:

- A review of market wins and woes in 2025

- A quick look at the themes and risks in 2026

- Traditional 401(k)/IRA vs Roth: what’s the difference?

A Look Back

2025 is officially in the books and markets logged another strong year, extending the annual winning streak to three years dating back to 2023. As always, the market had a wall of worry to contend with, potential disruptions that tempt investors to stray from their plan. We saw the presidency change hands, wars in Eastern Europe and the Middle East, rising tensions in South America, and a dramatic new tariff plan that was (and still is) constantly changing.

Despite the setbacks, stocks finished the year solidly in the green. The Dow Jones finished the year up 13.22%, the S&P 500 up 15.41%, and the NASDAQ up 18.42%. However, the markets had their share of worrying moments. The biggest challenge of the year was when President Trump unveiled his new tariff plan on April 2nd, dubbed by the President as “Liberation Day”. Markets were aware of a potentially disruptive tariff plan in the works and had been selling off since mid-February but really stepped on the gas once the actual plan was unveiled.

From the all-time highs on February 18th to the day Trump announced a 90-day pause on April 8th, the Dow Jones fell 15.09%, the S&P 500 fell 18.71% and the NASDAQ fell 22.14%. Really sit and digest those numbers for a second: if you were invested in these broad US stock indexes, you saw your investments fall 15, 18 or 22 percent in six weeks. Tariff fears largely receded as President Trump and his team negotiated trade deals with certain countries and the Supreme Court struck down other parts of the plan.

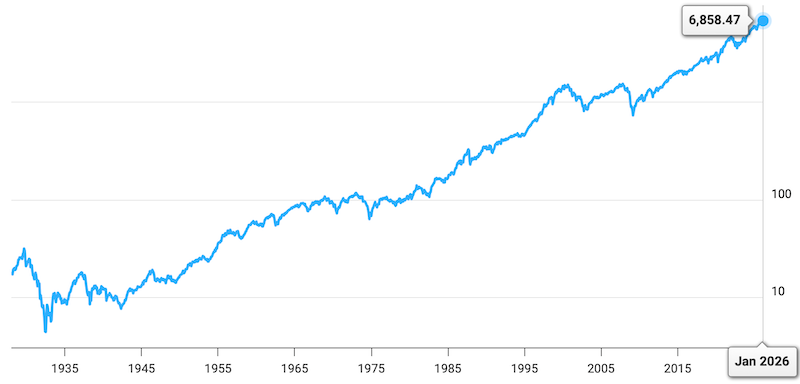

Now think about this: from the lows of the year on April 8th to the end of the year, the Dow Jones gained 28.52%, the S&P 500 gained 37.64% and the NASDAQ gained a staggering 52.19%. THIS IS WHY it is so critical to keep from panicking when stocks fall. A panic-sale on April 8th would have locked in a loss of 15-22% and prevented you from participating in a powerful rally. Staying the course when markets get choppy is easier said than done; personally, I think this 100-year chart of the S&P 500 is a great reminder to stay focused on the long-term and worry less about the day-to-day disruptions:

(source: MacroTrends)

A Look Ahead

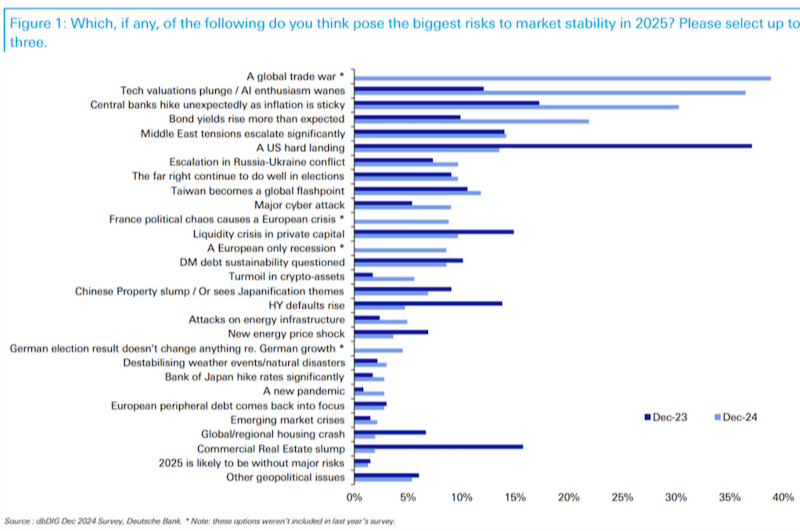

Every year brings new opportunities and risks to the investment markets. An interesting quirk of market risks is that investors are surprisingly poor at predicting them; after all, the real risks are things that you don’t see coming. For example, look at this survey of professional investors from the end of 2024, asking what the biggest risks will be in 2025:

(source: Deutsche Bank)

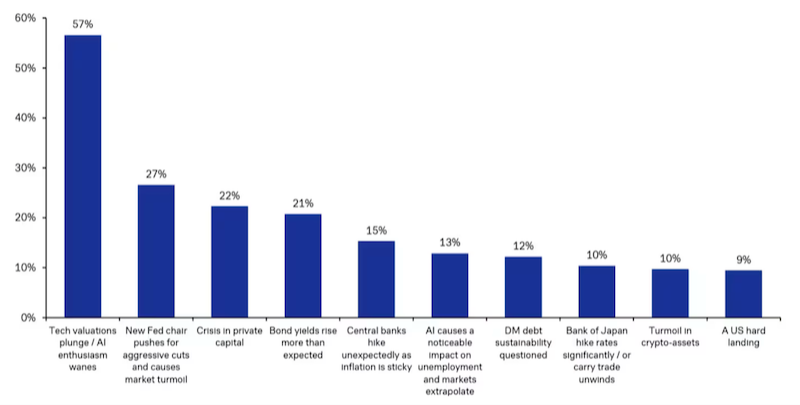

Interestingly, this survey did correctly predict that a trade war (tariffs) would be the biggest risk in 2025. However, look through some of the other top risks listed. Tech valuations plunge (wrong), interest rate hikes (wrong), a US hard landing/recession (wrong), etc. I’m pointing this out so you will take the following chart with a grain of salt; here is the same firm’s survey for risks in 2026:

(source: Deutsche Bank)

Clearly the biggest fear for investors this year is that AI enthusiasm will fall and tech stock prices will follow suit. I can’t predict the future so I can’t tell you definitively whether the AI trade will keep working or not, although personally I believe it will continue to be a boost for markets. I *am* confident that this is not (yet) a bubble in the traditional sense; for anyone who missed my Boom or Bubble newsletter from November, I will be sending it out tomorrow as a standalone article to everyone subscribed to the newsletter.

Of course there are other risks on the list: a change in Federal Reserve policy under a new chairman, AI advances pushing people out of their jobs, midterm elections in November, etc. The important thing to remember is that short-term disruptions are exactly that, short-term, and the best decision for the long-term is staying the course.

Traditional vs. Roth

One of the most common questions we receive here at Eternal Wealth Management is regarding traditional 401(k)s and IRAs vs. their Roth counterparts. There are a few rules differences surrounding each, but the main difference is their tax treatment. Here’s the easiest way to remember the difference: traditional 401(k)s & IRAs are taxedat the end, whereas Roths are taxedupfront.

When you contribute funds to a traditional 401(k) or IRA*, those funds are subtracted from your taxable income, meaning you are not being taxed on that income for that year (*this may not apply to IRAs if your income is too high or a few other scenarios). Your funds go into the 401(k) or IRA pre-tax, grow tax-deferred (no taxes on trades), and then is taxed as ordinary income when you pull funds in retirement. There is also a 10% penalty for pulling funds before age 59½ (with a few exceptions).

Roths are the opposite: you put in after-tax funds (meaning no tax deduction for the year you contribute the funds), still grow tax-deferred, and then is tax-free when you pull funds in retirement. Additionally, you are able to withdraw your basis (funds which you contributed) without a penalty before retirement.

You may be asking “which one is better?” Truthfully the answer is different for everyone. A worker in a very high-income tax bracket may elect to contribute solely to their traditional 401(k) and/or IRA to reduce their current taxes. A different worker may be expecting high retirement income from pensions or other sources and would like a Roth to not raise their retirement tax bill more. There is no one-size-fits-all strategy with these accounts, they are simply tools in the toolkit to most efficiently plan for retirement. If you have any questions about what would be best for your own situation, please reach out to us and we will be more than happy to help.

What Else

- President Trump announced the capture of Venezuelan President Nicolás Maduro, marking a new level of tensions with the South American country

- Ukrainian President Volodymyr Zelenskyy said that Ukraine and the US are 90% of the way to a ceasefire deal with Russia

- A fire in Switzerland killed at least 40 revelers at a bar during New Year’s Eve celebrations

- Protests in Iran have reached a boiling point, and President Trump has vowed to back the protesters if the Iranian government uses lethal force against them

- Ole Miss plays Miami in the College Football semifinal tomorrow night at 6:30 PM CT on ESPN

- Oregon plays Indiana in the College Football semifinal Friday night at 6:30 PM on ESPN

What We’re Reading

NASA is sending astronauts on a trip to the moon this year, perhaps as early as February. The Artemis II mission will send four spacefarers to orbit the moon in the closest visit in more than 50 years. The mission is not planning a landing on the moon but is part of a larger project to build sustainable infrastructure on the moon by 2030. Click below to learn more about the mission:

What’s Happening Downtown

The Myriad Gardens is hosting Chefs in the Garden – Bread in a Bag this Saturday, January 10th. This is a family-friendly event where kids can learn the basics of baking their own bread! The event runs from 2:00-3:00 PM and costs $15 ($12 for Myriad Gardens members). Click below to learn more and register for the event:

To read more from our blog, click here

Written by: Kane Ogle, CFP®

Steve Beck, Kane Ogle, CFP®, Amber Eduvigen, CFP®, Cale Olbert, CFP®, Brett Valentine, CFP®, Brandon Ingerson, Bill Daniel, Sam Postich, Jenni Hess